Unveiled : GHG Protocol Land Sector and Removals

Carbon accounting provides a compass to businesses in their quest for climate stewardship. It is a living, evolving field that improves and adapts. With this in mind, we share some of the most important recent developments in the field. First, the most widely applied standard of greenhouse gas accounting, the GHG Protocol, has special new guidance. After years of development, the GHG Protocol Land Sector and Removals (GHGP LSR) was published in late January 2026. The document is 133 pages long; we read it so you don’t have to. The document directs companies how to account for GHG emissions and CO2 removals from agriculture as well as CO2 removals through technology.

This is an important development since land use contributes nearly a quarter of global emissions, according to the best assessments. Although accounting for global emissions across billions of hectares of complex living systems is very different than the clear and simple crunching numbers for fuel combustion, the rigorous attempts to account at company and country levels for land-based emissions are very important due to their sizable impact.

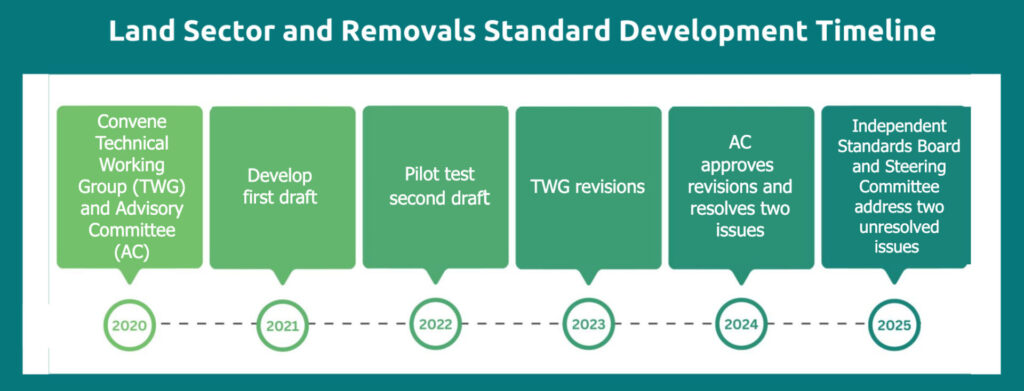

Part of the fanfare over GHGP LSR release has to do with the length of time (five years) over which the guidance has been developed, in these thoughtfully designed phases:

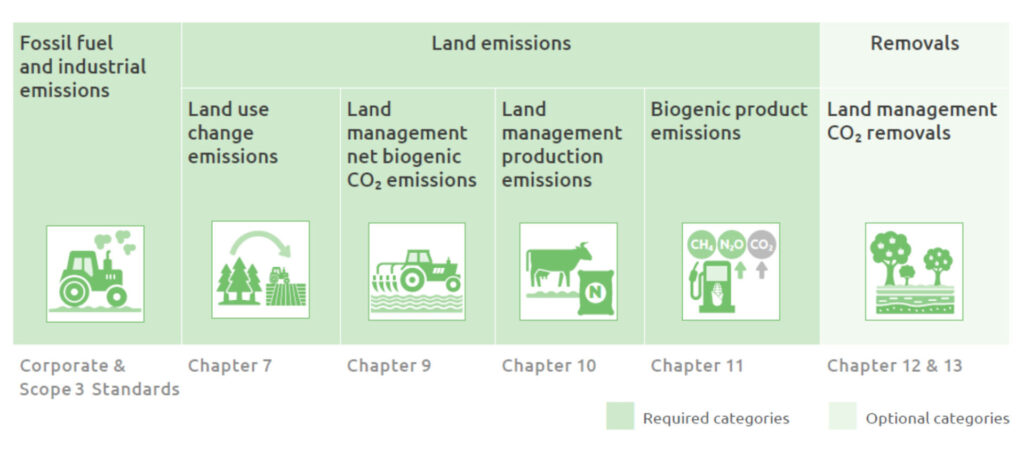

The structure of GHGP LSR guidance is shown below, highlighting the different areas that are in its scope, per the 17-page executive summary:

Each of the different emission areas will be accounted for separately. In some cases, it will require breaking apart numbers that had bundled fossil-based and land-based emissions. In other cases, new accounting processes will be needed.

Note:

- Forestry is not yet included, even if it was in earlier drafts. The intention is to add it in the future.

- If you are committed to SBTs as part of your business strategy around credible decarbonization, this guidance is the accounting counterpart to SBTi’s FLAG targets. Best practice is to now use this guidance for your FLAG-related accounting, as Climate Positive is with its clients.

How are you integrating this new guidance into your work?

What has your experience been thus far? Please let us know.

New & Updated Standards in the Dynamic Carbon Landscape

While the GHG Protocol (GHGP) is the best known and most widely used standard of carbon accounting, it is just one standard in a field with other noteworthy methods that are currently under development. Other changes to established standards and new proposed standards and frameworks important to share:

GHG Scope 2. Governs GHG accounting for electricity. As proposed, changes emphasize use of shorter interval (monthly or even hourly data) over the from annual average data currently used.

SBTi Corporate Net Zero v2. Shakes up the state of target setting if any of several proposed changes go through: separate scope 1 target (headwind), scope 2 low-carbon electricity alignment rather than emission reduction targets, focus on subset of major scope 3 categories (tailwind) and more.

Task Force for Corporate Accounting Transparency (TCAT). Complements GHGP and SBTi with an array of disclosures (statements) for carbon-related interventions, whether or not those interventions are in your value chain. GHGP and SBTi focus heavily on the value chain.

Exponential Roadmap Climate Solutions. Recognizes carbon excellence at the product and organizational levels. We like it as it provides a pathway to recognize already-leading products and companies, rather than requiring those companies to make dramatic emission reductions after they’ve already achieved excellent performance.

Futerra/Univ. of Oxford Spheres of Influence. Recognizes business activities that fall through the GHGP and SBTi cracks: R&D/product development, project finance, policy and advocacy. These activities are frequently leading indicators of decarbonization, and frequently set the stage for climate efforts to succeed or fail. Scrutiny of these activities is well-deserved.

The extent to which new standards gain transaction is one key issue to watch. Keep an eye out for our future reporting on these fronts!

Have questions on SBTi targets or corporate carbon emissions? Contact us here , or on LinkedIn.